On June 1, 2020, the Cabinet Committee on Economic Affairs approved a revision in the definition of Micro, Small and Medium Enterprises (MSMEs).[1] In this blog, we discuss the change in the definition as approved by the Cabinet, and examine some of the common criteria used for classification of MSMEs.

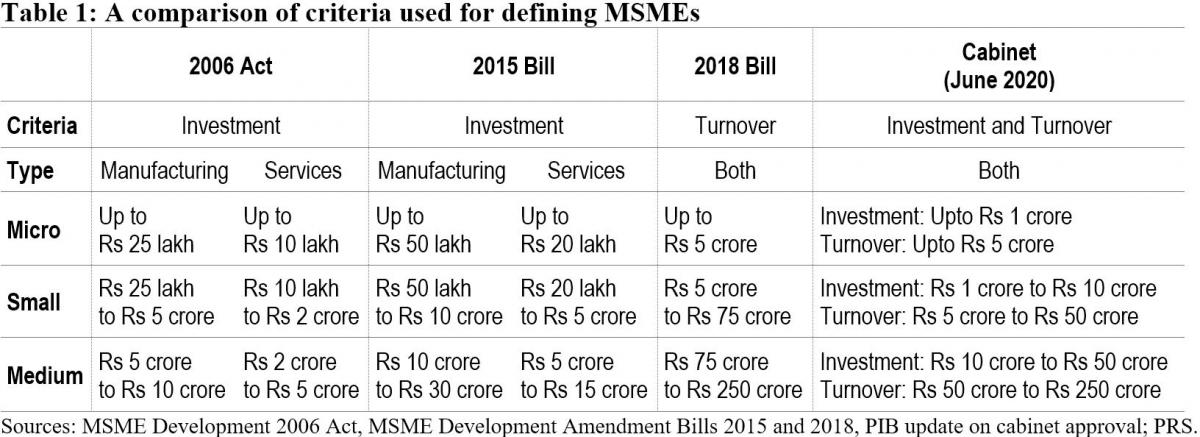

Currently, MSMEs are defined under the Micro, Small and Medium Enterprises Development Act, 2006.[2] The Act classifies them as micro, small and medium enterprises based on: (i) investment in plant and machinery for enterprises engaged in manufacturing or production of goods, and (ii) investment in equipment for enterprises providing services. As per the Cabinet approval, the investment limits will be revised upwards and annual turnover of the enterprise will be used as additional criteria for the classification of MSMEs (Table 1).

Earlier attempts to amend the definition of MSMEs

The central government has sought to revise the definition of MSMEs in the Act on two earlier occasions. The government introduced the MSME Development (Amendment) Bill, 2015 which proposed to increase the investment limits for manufacturing and services MSMEs.[3] This Bill was withdrawn in July 2018 and another Bill was introduced. The MSME Development (Amendment) Bill, 2018 proposed to: (i) use annual turnover as criteria instead of investment for classification of MSMEs, (ii) remove the distinction between manufacturing and services, and (iii) provide the central government with the power to revise the turnover limits, through a notification.[4] The 2018 Bill lapsed with the dissolution of 16th Lok Sabha.

Global trends in criteria for the classification of MSMEs

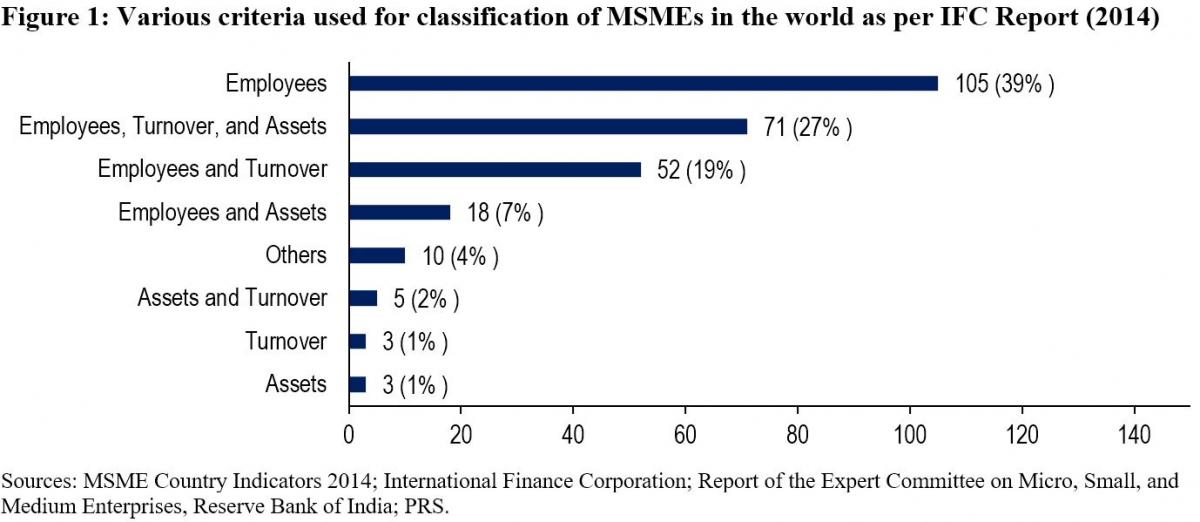

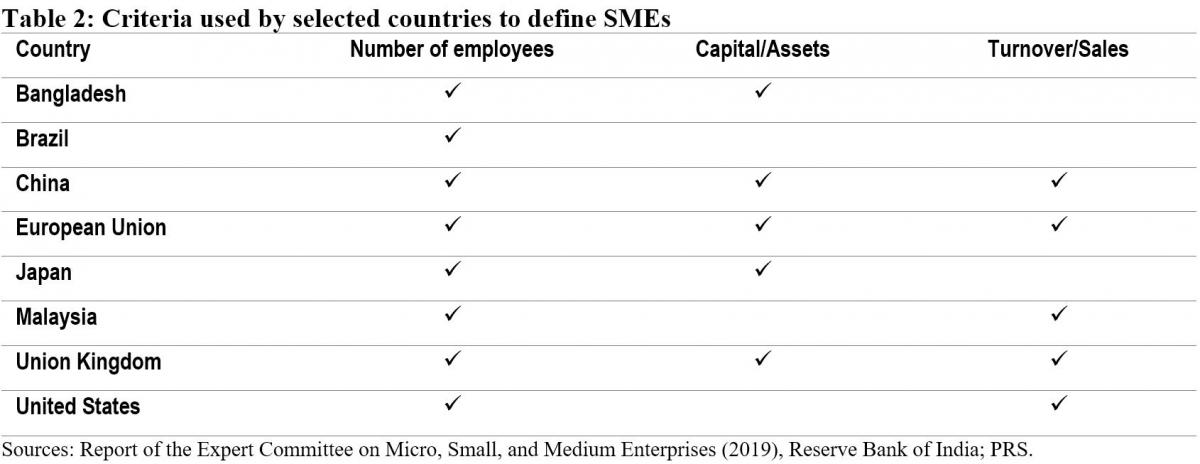

While India will now be using investment and annual turnover as the criteria to classify MSMEs, globally, the number of employees is the most widely used criteria for classifying MSMEs. The Reserve Bank of India's Expert Committee on MSMEs (2019) cited a study by the International Finance Corporation in 2014 which analysed 267 definitions used by different institutions in 155 countries.[5],[6] According to the study, countries used a combination of criteria to classify MSMEs. 92% of the definitions used the number of employees as one of the criteria. Other frequently used criteria were: (i) turnover (49%), and (ii) value of assets (36%). 11% of the analysed definitions used alternative criteria such as: (i) loan size, (ii) years of experience, and (iii) initial investment.

Evaluation of common criteria used to define MSMEs

Investment: The 2006 Act uses investment in plant, machinery, and equipment to classify MSMEs. Some of the issues with the investment criteria include:

Due to their informal and small scale of operations, firms often do not maintain proper books of accounts and hence find it difficult to get classified as MSMEs as per the current definition.5

The investment-based classification incentivises promoters to keep the investment size restricted to retain the benefits associated with the micro or small category.7

Turnover: The 2018 Bill sought to replace the investment criteria with annual turnover as the sole criteria for the classification of MSMEs. The Standing Committee agreed with the proposal under the Bill to use annual turnover as the criteria instead of investment.7 It observed that this could overcome some of the shortcomings of classification based on investment. While turnover based criteria will also require verification, the Committee noted that the GST Network (GSTN) data can act as a reliable source of information for this purpose. However, it also observed that:7

With turnover as a criterion for classification, corporates may misuse the incentives meant for MSMEs. For instance, there is a possibility that a multi-national company may produce a large quantity of products worth a high turnover and then market it through various subsidiaries registered as Micro or Small enterprise under GSTN.

The turnover of some enterprises may fluctuate depending on their business, which may result in the change of classification of the enterprise during a year.

The Committee noted that there is a wide gap in turnover limits. For instance, an enterprise with a turnover of Rs 6 crore and an enterprise with a turnover of Rs 75 crore (as proposed in 2018 Bill) would both be classified as a small enterprise, which seems incongruous.

The Expert Committee (RBI) also recommended using annual turnover as the criteria for classification instead of investment.5 It observed that turnover based definition would be transparent, progressive, and easier to implement through the GSTN. It also recommended that the power to change the definition of MSMEs should be delegated to the executive as it will help in responding to changing economic scenarios.

Number of employees: The Standing Committee had highlighted that in a labour-intensive country like India, appropriate focus is required on employment generation and MSME sector is the most suitable platform for this.7 It had recommended that the central government should assess the number of persons employed in the MSME sector and also consider employment as a criterion while classifying MSMEs. However, the Expert Committee (RBI) stated that while the employment-based definition is an additional feature preferred in some countries, the definition would pose challenges in implementation.5 According to the Ministry of MSME, employment as a criterion has problems due to: (i) factors such as seasonality and informal nature of engagement, (ii) similar to investment criteria, this would also require physical verification and has associated cost overheads.7

Number of MSMEs

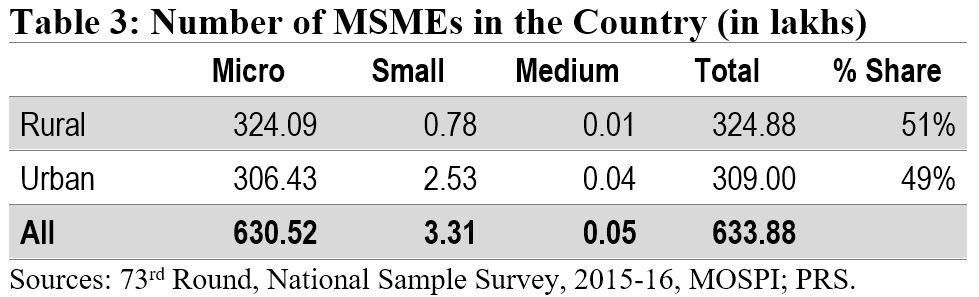

According to the National Sample Survey (2015-16), there were around 6.34 crore MSMEs in the country. The micro sector with 6.3 crore enterprises accounted for more than 99% of the total estimated number of MSMEs. The small and medium sectors accounted for only 0.52% and 0.01% of the estimated number of enterprises, respectively. Another dataset to understand the distribution of MSMEs is Udyog Aadhaar, a unique identity provided by the Unique Identification Authority of India (UIDAI) to MSME enterprises.[8] Udyog Aadhaar registration is based on self-declaration by enterprises. Between September 2015 and June 2020, 98.6 lakh enterprises have registered with UIDAI. According to this dataset, micro, small, and medium enterprises comprise 87.7%, 11.8% and 0.5% of the MSME sector respectively.

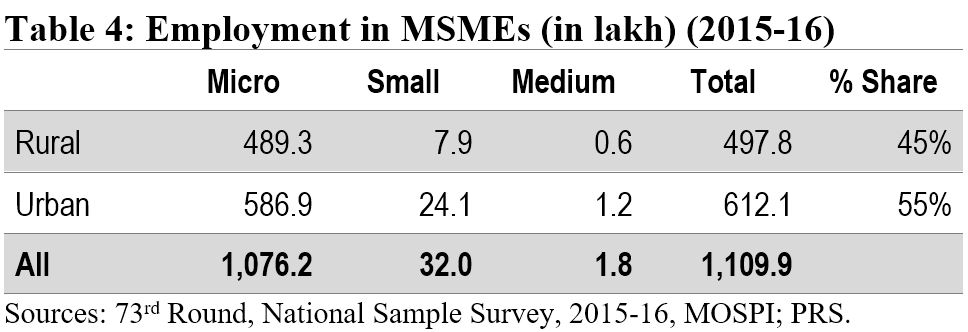

Employment in the MSME sector

The MSME sector employed nearly 11.1 crore people in 2015-16. The sector was the second largest employer after the agriculture sector. The highest number of employed persons were engaged in trade activity (35%), followed by persons engaged in manufacturing (32%).

Implications of change in the definition of MSMEs

The change in the definition of MSMEs may result in many enterprises which are currently classified as Small enterprises be reclassified as Micro, and those classified as Medium enterprises be reclassified as Small. Further, there may be many enterprises which are not currently classified as MSMEs, which may fall under the MSME classification as per the new definition. Such enterprises will also now benefit from the schemes related to MSMEs. The Ministry of MSME runs various schemes to provide for: (i) flow of credit to MSMEs, (ii) support for technology upgrade and modernisation, (iii) entrepreneurship and skill development, and (iv) cluster-wise measures to promote capacity-building and empowerment of MSME units. For instance, under the Credit Guarantee Fund Scheme for Micro and Small Enterprises, a credit guarantee cover of up to 75% of the credit is provided to micro and small enterprises.[9] Thus, the re-classification may require a significant increase in budgetary allocation for the MSME sector.

Other announcements related to MSMEs in the aftermath of COVID-19

MSME sector accounted for nearly 33.4% of the total manufacturing output in 2017-18.[10] During the same year, its share in the country’s total exports was around 49%. Between 2015 and 2017, the contribution of the sector in GDP has been around 30%. Due to the national lockdown induced by COVID-19, businesses including MSMEs have been badly hit. To provide immediate relief to the MSME sector, the government announced several measures in May 2020.[11] These include: (i) collateral-free loans for MSMEs with up to Rs 25 crore outstanding and up to Rs 100 crore turnover, (ii) Rs 20,000 crore as subordinate debt for stressed MSMEs, and (iii) Rs 50,000 crore of capital infusion into MSMEs. These measures have also been approved by the Union Cabinet.[12]

For more details on the announcements made under the Aatma Nirbhar Bharat Abhiyan, see here.

[1] “Cabinet approves Upward revision of MSME definition and modalities/ road map for implementing remaining two Packages for MSMEs (a)Rs 20000 crore package for Distressed MSMEs and (b) Rs 50,000 crore equity infusion through Fund of Funds”, Press Information Bureau, Cabinet Committee on Economic Affairs, June 1, 2020.

[2] The Micro, Small and Medium Enterprises Development Act, 2006, https://samadhaan.msme.gov.in/WriteReadData/DocumentFile/MSMED2006act.pdf.

[3] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2015, https://www.prsindia.org/sites/default/files/bill_files/MSME_bill%2C_2015_0.pdf.

[4] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2018, https://www.prsindia.org/sites/default/files/bill_files/The%20Micro%2C%20Small%20and%20Medium%20Enterprises%20Development%20%28Amendment%29%20Bill%2C%202018%20Bill%20Text.pdf.

[5] Report of the Expert Committee on Micro, Small and Medium Enterprises, The Reserve Bank of India, July 2019, https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/MSMES24062019465CF8CB30594AC29A7A010E8A2A034C.PDF.

[6] MSME Country Indicators 2014, International Finance Corporation, December 2014, https://www.smefinanceforum.org/sites/default/files/analysis%20note.pdf.

[7] 294th Report on Micro Small and Medium Enterprises Development (Amendment) Bill 2018, Standing Committee on Industry, Rajya Sabha, December 2018, https://rajyasabha.nic.in/rsnew/Committee_site/Committee_File/ReportFile/17/111/294_2019_3_15.pdf.

[8] Enterprises with Udyog Aadhaar Number, National Portal for Registration of Micro, Small & Medium Enterprises, Ministry of Micro, Small and Medium Enterprises, https://udyogaadhaar.gov.in/UA/Reports/StateBasedReport_R3.aspx.

[9] Credit Guarantee Fund Scheme for Micro and Small Enterprises, Ministry of Micro, Small and Medium Enterprises, http://www.dcmsme.gov.in/schemes/sccrguarn.htm.

[10] Annual Report 2018-19, Ministry of Micro, Small and Medium Enterprises, https://msme.gov.in/sites/default/files/Annualrprt.pdf.

[11] "Finance Minister announce measures for relief and credit support related to businesses, especially MSMEs to support Indian Economy’s fight against COVID-19", Press Information Bureau, Ministry of Finance, May 13, 2020.

[12] "Cabinet approves additional funding of up to Rupees three lakh crore through introduction of Emergency Credit Line Guarantee Scheme (ECLGS)", Press Information Bureau, Ministry of Finance, May 20, 2020.

On June 13, 2022, the West Bengal government passed a Bill to replace the Governor with the Chief Minister, as the Chancellor of 31 state public universities (such as Calcutta University, Jadavpur University). As per the All India Survey on Higher Education (2019-20), state public universities provide higher education to almost 85% of all students enrolled in higher education in India. In this blog, we discuss the role of the Governor in state public universities.

What is the role of the Chancellor in public universities?

State public universities are established through laws passed by state legislatures. In most laws the Governor has been designated as the Chancellor of these universities. The Chancellor functions as the head of public universities, and appoints the Vice-Chancellor of the university. Further, the Chancellor can declare invalid, any university proceeding which is not as per existing laws. In some states (such as Bihar, Gujarat, and Jharkhand), the Chancellor has the power to conduct inspections in the university. The Chancellor also presides over the convocation of the university, and confirms proposals for conferring honorary degrees. This is different in Telangana, where the Chancellor is appointed by the state government.

The Chancellor presides over the meetings of various university bodies (such as the Court/Senate of the university). The Court/Senate decides on matters of general policy related to the development of the university, such as: (i) establishing new university departments, (ii) conferring and withdrawing degrees and titles, and (iii) instituting fellowships.

The West Bengal University Laws (Amendment) Bill, 2022 designates the Chief Minister of West Bengal as the Chancellor of the 31 public universities in the state. Further, the Chief Minister (instead of the Governor) will be the head of these universities, and preside over the meetings of university bodies (such as Court/Senate).

Does the Governor have discretion in his capacity as Chancellor?

In 1997, the Supreme Court held that the Governor was not bound by the aid and advice of the Council of Ministers, while discharging duties of a separate statutory office (such as the Chancellor).

The Sarkaria and Puunchi Commission also dealt with the role of the Governor in educational institutions. Both Commissions concurred that while discharging statutory functions, the Governor is not legally bound by the aid and advice of the Council of Ministers. However, it may be advantageous for the Governor to consult the concerned Minister. The Sarkaria Commission recommended that state legislatures should avoid conferring statutory powers on the Governor, which were not envisaged by the Constitution. The Puunchi Commission observed that the role of Governor as the Chancellor may expose the office to controversies or public criticism. Hence, the role of the Governor should be restricted to constitutional provisions only. The Statement of Objects and Reasons of the West Bengal University Laws (Amendment) Bill, 2022 also mentions this recommendation given by the Puunchi Commission.

Recent developments

Recently, some states have taken steps to reduce the oversight of the Governor in state public universities. In April 2022, the Tamil Nadu Legislative Assembly passed two Bills, to transfer the power of appointing the Vice-Chancellor (in public universities) from the Governor, to the state government. As of June 8, 2022, these Bills have not received the Governor’s assent.

In 2021, Maharashtra amended the process to appoint the Vice Chancellor of state public universities. Prior to the amendment, a Search Committee forwarded a panel of at least five names to the Chancellor (who is the Governor). The Chancellor could then appoint one of the persons from the suggested panel as Vice-Chancellor, or ask for a fresh panel of names to be recommended. The 2021 amendment mandated the Search Committee to first forward the panel of names to the state government, which would recommend a panel of two names (from the original panel) to the Chancellor. The Chancellor must appoint one of the two names from the panel as Vice-Chancellor within thirty days. As per the amendment, the Chancellor has no option of asking for a fresh panel of names to be recommended.